Introduction

The Fifth Circuit recently ruled that the Federal Communications Commission’s (FCC) Universal Service Fund (USF) assessments are unconstitutional, contradicting other circuit courts that said they were fine. Since the circuits disagree, the case will likely go to the Supreme Court. We are not lawyers so will not speculate about the myriad ways that the Supremes could decide. Instead, we provide evidence and considerations for a more rational and effective system to achieve “universal service” goals.

While we do not want to minimize the disruption likely to occur if the USF were cut off cold turkey, the Circuit court ruling presents an opportunity to confront two very real problems that need to be addressed: funding and spending.

- The way the program is funded is inefficient, unsustainable, and regressive. Regardless of the judicial outcome, the tax that the court declared unconstitutional is both inefficient, by taxing a small, price-sensitive, declining base, and regressive, with a higher proportional burden falling on those least able to afford it.

- The program spends too much money on the wrong things.

- The High Cost Fund in particular, which accounts for about half of total spending, is outdated and wasteful. Research shows that it has not made much of a difference in connecting households despite billions of dollars spent every year for the past 25 years. Additionally, new terrestrial and satellite fixed wireless technologies challenge the fundamental idea of “high cost” areas since satellite in particular entails the same costs everywhere.

- The Universal Service Administrative Corporation (USAC) – the organization the FCC created to manage the USF – has increased its administrative expenses from $105 million in 2010 to $204 million in 2020 to $365 million in 2023 while program expenditures stayed fairly constant.

Solutions to both of these problems are straightforward:

- Expand the tax base. Funding the program from general government revenues, as Congress did with the Affordable Connectivity Program, is more efficient and less regressive than the current system.

- Reduce the size of the fund substantially. Satellite and wireless providers are likely to be able serve higher cost areas with much lower, if any, subsidy.

The Tax to Raise the Money for the USF Is Inefficient, Unsustainable, and Regressive

Regardless of the final decision about its constitutionality, the current mechanism for funding the USF is fundamentally flawed by any measure of the right way to tax.

Taxes always entail economic costs (deadweight loss) by distorting behavior. That is not an argument against taxes–we want the government to provide services. But it is an argument for making the cost of a tax as small as possible. Effective taxation aims to minimize behavioral distortions by broadening the tax base and targeting less price-sensitive goods and activities. The USF tax, by contrast, taxes a narrow base of price-sensitive behavior.

Additionally, as a society we generally believe that lower-income people should pay a proportionately smaller tax rate than higher-income people; hence, our progressive income tax system. The USF tax burden falls disproportionately on lower-income people.

The USF Tax System Is Incoherent

In the 1996 Telecommunications Act, Congress gave the FCC the ability to tax interstate and international “telecommunications” service revenue. Over time, however, those revenues (aka, the tax base) have dwindled as more of the revenue from communications services is allocated to data or “information” services. As the reality of communications changed, the FCC has engaged in painful contortions to assign revenues to interstate and international telecommunications. 30 years ago, wireless phones were used almost exclusively for traditional voice calls and revenues could be allocated almost entirely to telecommunications services. Today, revenues from a $30 cell phone plan that offers unlimited calling, data, and text can be allocated in many ways across those services, with much less going toward voice service as people use other services more and more. As a result, today the FCC uses a complicated algorithm to decide how much of a company’s revenues it considers “interstate” or “international” “telecommunications” revenues for the purpose of USF taxes.

The Tax Base is Too Small to Support the Fund and Decreasing, Making the Fund Unsustainable

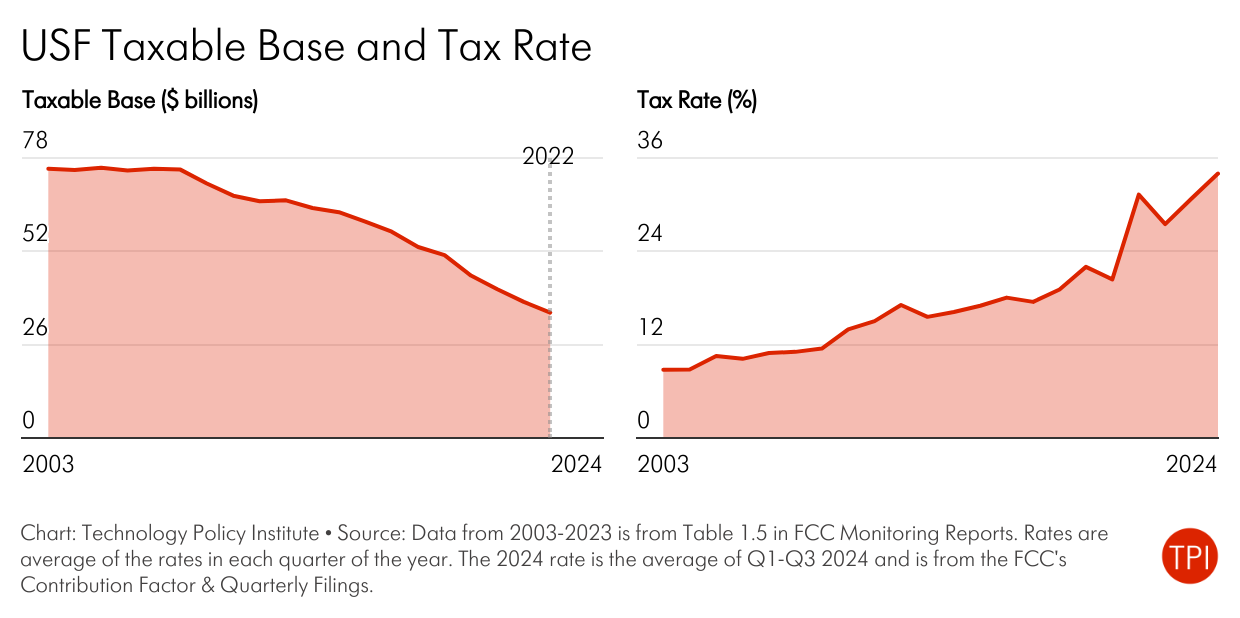

The taxable base for telecommunications services has steadily declined from $70 billion in 2003 to $30 billion in 2022, a decrease of more than 50%. This decline is due to consumers having multiple means of communication, many of which are free, making them inclined to use taxed services less. The figure below shows that as the pool of taxable telecommunication revenues decreased with the move to more data usage, the FCC has had to increase the tax rate from 14% in 2010 to over 34% in 2024 to maintain the revenues spent by the Universal Service Fund (USF).

The high tax rate creates a destructive cycle that threatens USF’s sustainability. It discourages users from making taxable communications, incentivizing consumers and producers to shift to non-taxable alternatives. Consumers increasingly opt for services like FaceTime and Zoom, which are classified as “information services” rather than “telecommunications services,” while providers have more justification to allocate revenues to these non-taxable categories. As the FCC increases tax rates to maintain revenue, it only strengthens these incentives, further shrinking the tax base and making the current USF model unsustainable.

The USF Tax is Regressive

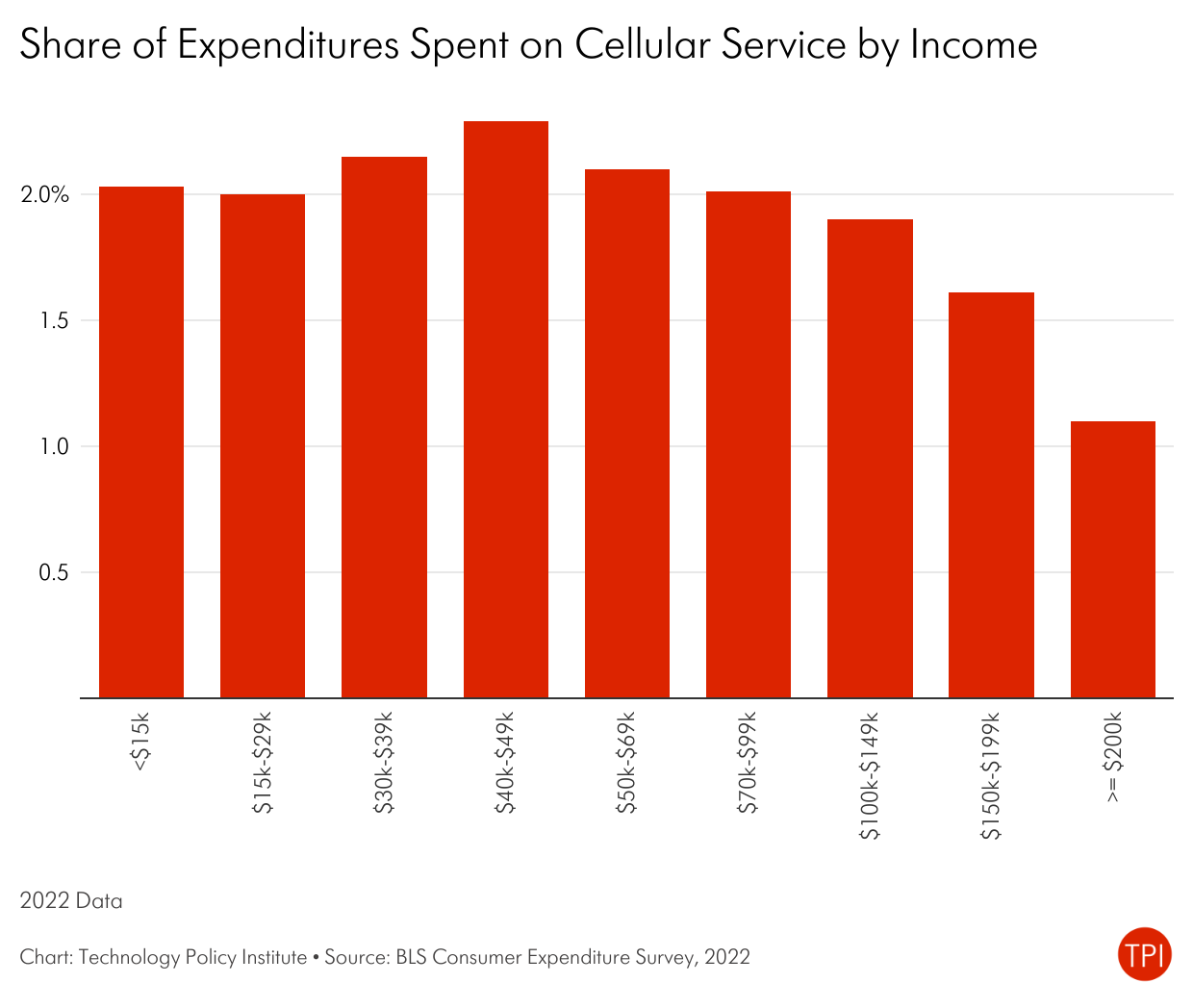

The USF tax rate is the same for all levels of income, unlike our progressive income tax system in which the rate increases with income. Additionally, lower-income people spend about twice as much as a share of their income on cellular service as do higher-income. The result is that the tax burden falls more heavily on lower-income people.

Some of this problem is mitigated by the Lifeline program, which provides a $9.25 per month subsidy to eligible households and also exempts them from paying the USF tax. Households that earn less than 135 percent of the poverty level or participate in a number of other low-income support programs, like SNAP, are eligible for Lifeline. However, that still leaves many lower-income people ineligible and therefore paying the tax. In addition, only about 20 percent of households eligible for Lifeline participate. As a result, the income share of the tax is higher on lower income households.

The USF Program Spends Too Much on the Wrong Things

The problem of how to pay for the USF becomes easier to solve the less the program spends, so a key objective is to avoid waste.

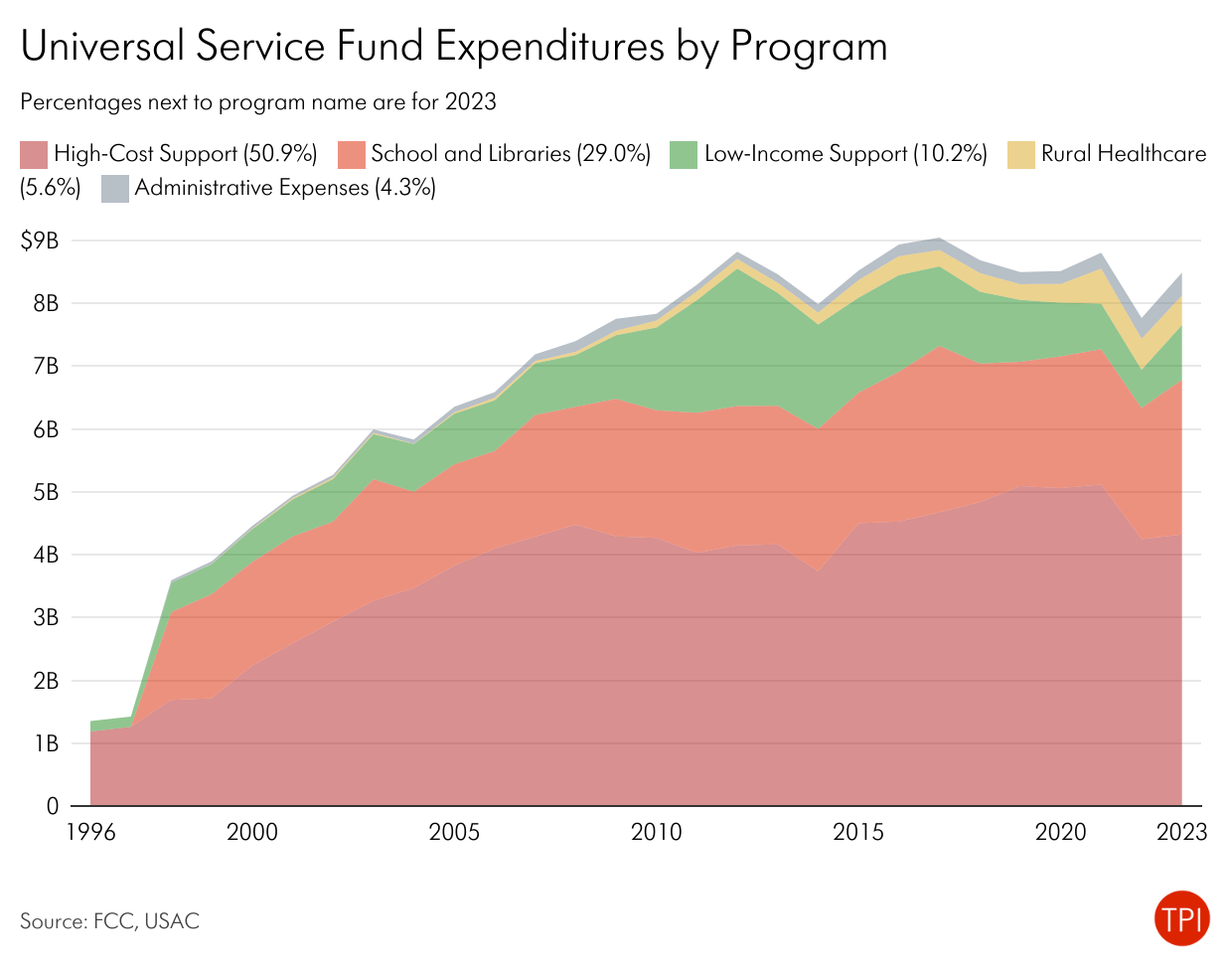

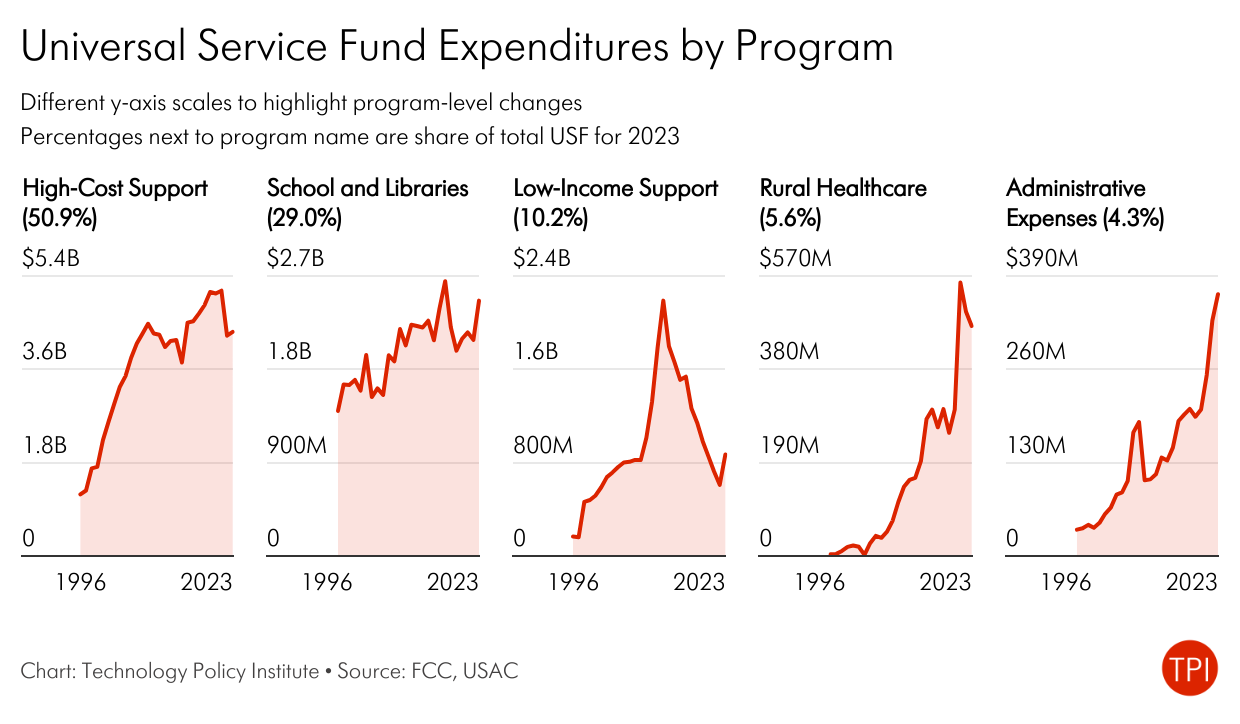

The Federal USF fund spends about $8 billion per year and has spent close to $200 billion in nominal dollars since 1995. The largest part of the fund, representing about half of the total at $4-$4.5 billion per year, is the High Cost Fund, intended to subsidize service in “high cost” areas. The figures below show a breakdown of spending over time by program. The first chart shows that it has remained relatively stable around $8 billion (in nominal terms) over the past 15 years. High-cost support (the lowest shaded region in the chart) accounts for about half of this amount each year.

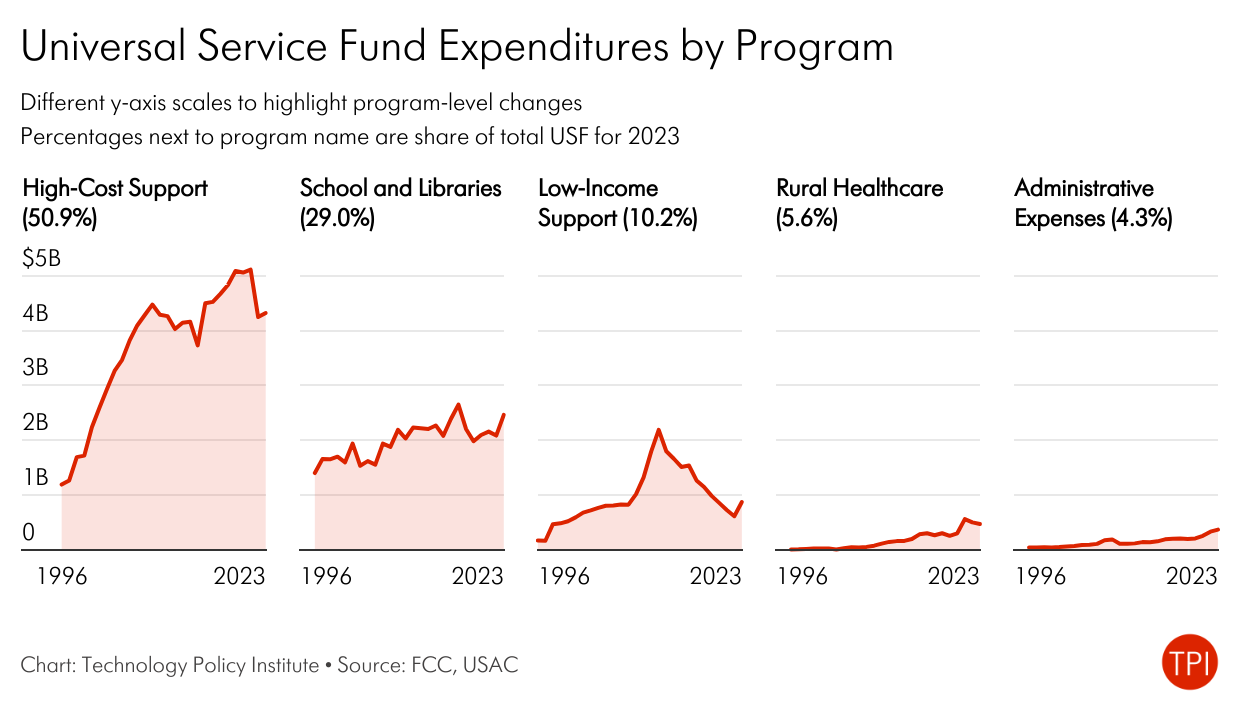

The two charts below provide a clearer view of the nominal expenditure by program from 1996 though 2023. The first chart uses the same vertical axis to make it easier to compare the sizes of the USF components. The second chart shows the same data, but with different vertical scales for each program to better see how each changed. High-cost support grew rapidly from 1996 through about 2008 and then leveled off. Low-income support grew rapidly from about 2011 though 2016 and then shrank rapidly. The other three parts of the program grew over time, especially in percentage terms as can be seen in the second set of graphs.

The High-Cost Fund is Too Large and Outdated

The Federal Universal service fund, especially the High Cost Fund, is too large. Improved service provided by terrestrial fixed wireless and low-earth orbiting satellites means it is possible to reach every household at lower cost, rendering even the phrase “high cost area” outdated.

While this assertion flies in the face of the typical “fiber-first” approach to broadband buildout, a key is to understand what quality of service is “necessary” to satisfy universal service. As the cost of deploying fiber increases with factors like topography and distance from existing networks, it becomes more likely that it is socially better to fund different technologies. Most internet services do not require more than about 50 mbps even for a family of four. Wireless service can deliver these speeds and higher in many cases, making it an option where it was not in the past. And while rural customers may not have the same quality reference as urban customers, consumer satisfaction surveys find that Starlink and T-Mobile Home Internet receive among the highest customer satisfaction ratings across ISPs. And wireless service has been improving over time, meaning that as bandwidth requirements increase, wireless may be able to serve households for the long-term.

Overhead Costs Have Ballooned

Operating a program entails expenses. However, spending on overhead by the Universal Service Administrative Company (USAC), which administers the USF programs, has grown from $105 million in 2010 to $204 million in 2020 to $365 million in 2023, while expenditures on universal service programs remained steady for more than a decade. As a point of comparison, the FCC’s entire budget request for 2023 was only slightly higher at about $390 million.

According to a recent GAO report, “USAC attributed the increase to replacing obsolete legacy systems and strengthening program integrity. For example, USAC doubled the number of staff working on one program to better combat waste, fraud, and abuse.” If this is the case, then we should expect to see these costs decrease. USAC should additionally be able to identify ways in which this additional staff has made the Fund more efficient.

Solutions: Reduce Spending and Revamp the Tax Mechanism

The USF needs to be revamped to reduce the inefficiencies it creates.

Make the Fund as Small as Possible–The Smaller the Fund, the Smaller the Problem

The High Cost Fund has outlived its usefulness, particularly as new technologies render even the term “high cost” nearly meaningless. Additionally, the $42 billion from the BEAD program, $10 billion from the Treasury Capital Projects Fund, and tens of billions from other Covid-era programs should provide additional coverage in areas that the High Cost fund inexplicably failed to cover despite its $200 billion history. Ramping down the High Cost Fund would cut the fund by about half.

To ensure that the Fund spends money effectively, its programs need to be evaluated, as the Government Accountability Office has repeatedly stated. Evaluations would help impose accountability, including for USAC’s overhead. Evaluation is not just compliance or guarding against fraud, although both are important. It is about testing whether the programs are having the effects we want them to have. It is worth acknowledging, too, that good evaluations could suggest increases in some parts of the program. For example, one could imagine increased low-income support, particularly if other programs are smaller.

Fund USF From General Government Revenues

The best solution, which is true regardless of the final court decision, is to fund USF out of general tax revenues. That would require annual Congressional appropriations. Congressional appropriations would have two benefits. First, the tax burden would be shared over a large base, meaning it would be relatively small and minimally distortionary. Second, it would create pressure to keep the size of the fund low and therefore for its programs to operate efficiently. The tradeoff would be less certainty than under the current system, but that argument applies to every government program. If the Department of Defense can live with annual appropriations, then the Universal Service Fund can, too.

Gregory Rosston is Director of the Public Policy Program at Stanford University and Senior Fellow at the Stanford Institute for Economic Policy Research. He is also a Lecturer in Economics and Public Policy at Stanford University where he teaches courses on competition policy and strategy, intellectual property, and writing and rhetoric. Rosston served as Deputy Chief Economist at the Federal Communications Commission working on the implementation of the Telecommunications Act of 1996 and he helped to design and implement the first ever spectrum auctions in the United States. He co-chaired the Economy, Globalization and Trade committee for the Obama campaign and was a member of the Obama transition team. He has served as a consultant to various organizations including the World Bank and the FCC, and as a board member and advisor to high technology, financial, and startup companies. Rosston received his Ph.D. in Economics from Stanford University specializing in the fields of Industrial Organization and Public Finance and his A.B. with Honors in Economics from University of California at Berkeley.

Scott Wallsten is President and Senior Fellow at the Technology Policy Institute and also a senior fellow at the Georgetown Center for Business and Public Policy. He is an economist with expertise in industrial organization and public policy, and his research focuses on competition, regulation, telecommunications, the economics of digitization, and technology policy. He was the economics director for the FCC's National Broadband Plan and has been a lecturer in Stanford University’s public policy program, director of communications policy studies and senior fellow at the Progress & Freedom Foundation, a senior fellow at the AEI – Brookings Joint Center for Regulatory Studies and a resident scholar at the American Enterprise Institute, an economist at The World Bank, a scholar at the Stanford Institute for Economic Policy Research, and a staff economist at the U.S. President’s Council of Economic Advisers. He holds a PhD in economics from Stanford University.